How to Choose the Right Disability Insurance Policy in 2025

The Most Overlooked Insurance in New York? Your Paycheck.

You ever been carry five grocery bags, rushing to the front door, begging to Zeus to lend his strength? Then, you feel a sharp pain in your arm. It’s nothing at first, a little ache, a quick stretch, and you’re back to scrolling your phone, thinking about what to make for dinner. But then it lingers. The pain the starts the grow. But you can’t let this stop you, you have work tomorrow.

Life doesn’t slow down when your body does. The rent’s still due. Groceries still need to be bought. Kids still need to be fed. And ambition doesn’t pay the bills if you’re stuck in bed.

So let me ask you something.

If your income stopped tomorrow, what would your life look like 30 days from now?

Would your savings hold? Would your family be okay? Would your plans survive?

Your body isn’t just your body, it’s your paycheck. Protecting your income might be the most important form of self-care that no one talks about.

That’s where disability insurance in comes in. Not as a luxury. As a lifeline.

So What Is Disability Insurance Really?

Imagine your walking across a tightrope high above the ground.

This tightrope, is your income. Every step (every paycheck) is a stride toward your goals: savings, dreams, rent, groceries, childcare.

Now imagine walking that tightrope with no safety net underneath you. One slip, a fall, a diagnosis, an accident, and everything you were building, can crash.

Disability insurance is that safety net.

It’s a financial product designed to protect your income if you’re unable to work due to illness or injury. Unlike workers' compensation, which only applies to job-related injuries, disability insurance covers both work and non-work-related health issues. That means whether you hurt your back lifting at a construction site or develop a serious illness that keeps you bedridden, disability insurance steps in.

Who actually needs it?

In short, anyone who relies on their income to pay the bills. That includes:

Freelancers and gig workers

Salaried employees

Self-employed professionals

Business owners

Most Americans are one or two missed paychecks away from serious financial hardship. Disability insurance ensures that even if you can’t work, you can still pay your rent, cover your utilities, and buy groceries. It typically replaces 50% to 70% of your income while you're unable to work, depending on the policy.

How long does it last?

That depends on the type of policy you have.

Short-term disability policies may last 3 to 6 months.

Long-term policies can extend for years or even until retirement.

And unlike workers' compensation, which is only available if your injury happened on the job, disability insurance can protect your income from any illness or injury that prevents you from working.

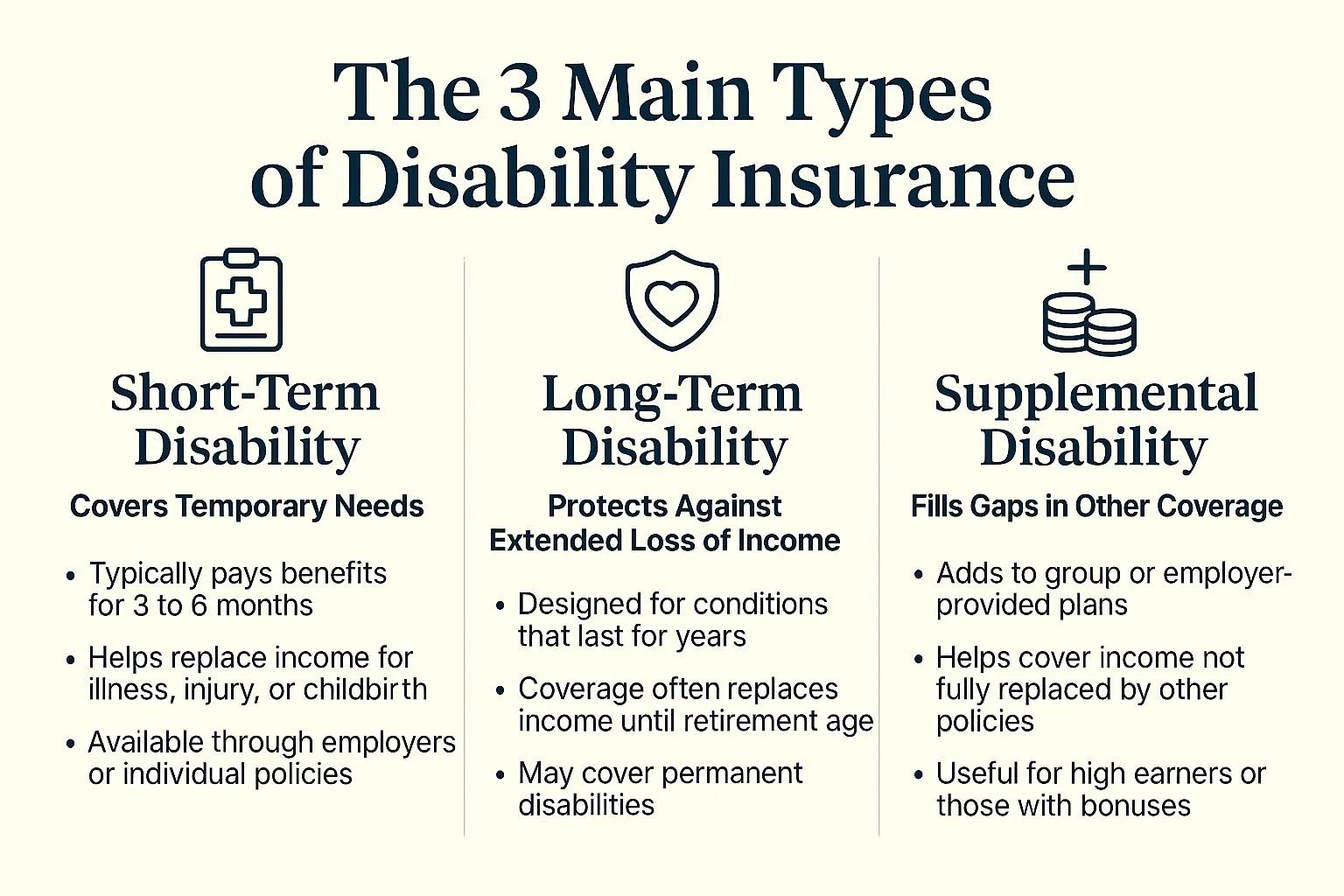

The 3 Main Types of Disability Insurance

Short-Term Disability Insurance

This is designed for immediate needs. Think of situations like:

Recovery from surgery

A broken limb

Complications from pregnancy

Severe illness like pneumonia or COVID

How does it work? Most short-term disability policies kick in within 7 to 14 days of your inability to work. They usually provide benefits for 3 to 6 months. Some plans may extend up to a year.

Where do you get it? Short-term disability is often provided through your employer. But if you're self-employed or your job doesn’t offer it, you can purchase it independently, though individual policies tend to cost more.

Pros:

Quick payout

Ideal for temporary conditions

Cons:

Coverage runs out quickly

May not cover all income sources (e.g., bonuses)

Long-Term Disability Insurance

This is for more serious, long-lasting health conditions:

Cancer

Stroke

Mental health disorders

Chronic illnesses

Serious injuries requiring long recovery

When does it start? Long-term disability often begins after short-term benefits run out—typically after 90 to 180 days.

How long does it last? Some policies last a few years, while others can last until retirement age (often 65 to 67).

Who needs it most?

High earners with significant monthly expenses

People with limited emergency savings

Entrepreneurs or freelancers with no employer plan

Pros:

Long-term financial security

Can cover a major loss of income over decades

Cons:

Higher premiums than short-term

Requires documentation and medical underwriting

Supplemental Disability Insurance

Let’s say you already have coverage through work. That’s great. But what if it only covers 50% of your base salary, ignores your commissions or bonuses, and gets taxed?

Supplemental disability insurance is designed to make sure you are fully covered. It can:

Increase your benefit amount

Extend the duration of your payout

Cover additional income like bonuses or variable compensation

Why is it important? Many employer policies don’t cover your total compensation. If you earn bonuses, commissions, or work overtime, those numbers might not be protected under a standard plan.

Can you buy it individually? Yes. Many private insurers offer supplemental disability plans tailored to professionals in different fields.

Pros:

Customizable to your financial needs

Provides more complete coverage

Cons:

Adds to your monthly insurance costs

Requires coordination with existing policies

Choosing the Right Plan for You

The right disability insurance policy depends entirely on your personal situation. Here are the big questions to consider:

Are you self-employed? If you run your own business or freelance, you likely don’t have any employer-sponsored coverage. You’ll want to build a personalized plan with long-term disability as the foundation.

Do you rely on a single income? If you're the sole breadwinner, even a short-term loss of income can be devastating. Consider layering both short and long-term coverage.

Do you work a physical job? Construction workers, nurses, dancers, your body is your career. One injury can sideline you. Look for plans that kick in quickly and offer comprehensive long-term support.

Do you have savings to fall back on? If you can cover 3 to 6 months of expenses, you might want a long-term policy with a longer waiting period (which often lowers your premium).

Employer vs. Individual Coverage

Here’s what most people don’t realize:

Employer-paid disability benefits are taxable. If your job gives you free disability insurance, any benefits you receive from that plan are considered taxable income. So if your policy promises to replace 60% of your salary, you may only net 45%-50% after taxes.

Individually paid disability benefits are tax-free. If you pay your own premiums out-of-pocket, the income you receive is yours, tax-free. That’s a big deal. It means your benefit amount is closer to your actual income.

Employer Plans Also Miss the Mark on Bonuses and Commissions Many employer policies are based on your base salary only. If you earn a large portion of your income from:

Bonuses

Overtime

Tips

Commission

…those earnings may not be protected.

This is where supplemental or individual plans can save the day. A personalized policy can be designed to reflect your real income, not just your W-2 base.

Pros and Cons of Employer Disability Insurance

Pros:

Usually free or low-cost

Easy to enroll (minimal paperwork)

Good starting point for basic coverage

Cons:

Taxable benefits

May not cover full income

Often non-transferable if you change jobs

Pros and Cons of Individual Disability Insurance

Pros:

Tax-free benefits

Portable (you keep it even if you switch jobs)

Can be tailored to your true income and needs

Cons:

Higher cost

Requires underwriting (medical and financial info)

How Much Does Disability Insurance Cost in 2025?

Premiums depend on a few key factors:

Your age and health

Your occupation

The length of the benefit period

The elimination period (how long you wait before benefits begin)

The percentage of income you want to replace

As a rule of thumb, disability insurance costs between 1% and 3% of your annual salary. So if you make $100,000, expect to pay $1,000 to $3,000 per year.

Can Freelancers and Gig Workers Get Covered?

Yes. In fact, they’re often the ones who need it most. If you’re a:

Musician

Creative professional

Rideshare driver

Coach or trainer

there are policies designed specifically for non-traditional workers. The process may involve proving your income through bank statements, invoices, or tax returns.

Protect Your Paycheck. Protect Your Peace of Mind.

You insure your home. You insure your car. You insure your phone.

But what about the thing that pays for all of it?

Your income is your foundation. It covers your rent or mortgage, puts food on the table, keeps the lights on, supports your kids, fuels your dreams. And yet, it’s the one thing most people forget to protect, until it’s too late.

Disability insurance isn’t about preparing for the worst. It’s about giving yourself space to recover when life throws a curveball. It’s about making sure that if your body takes a hit, your finances don’t face the same hit.

So here’s the truth in plain English:

Short-term disability insurance helps with recovery from temporary setbacks: injuries, illness, maternity leave.

Long-term disability insurance protects your income if something more serious keeps you out of work for years or forever.

Supplemental disability insurance fills in the gaps that your employer plan might miss, like bonuses, overtime, or commissions.

Employer coverage is great, but the benefits are taxable and often don’t cover your full income. Personal coverage is tax-free and customizable.

If you’re self-employed, in a physical job, or relying on a single income, the right policy can literally save your future.

You don’t need to be scared, you just need to be prepared.

At SJM Cares, we help people all over New York (and across the country) get the coverage they need without the pressure, the jargon, or the guesswork.

If you’re unsure where to start, we’ll walk you through it.

Ask the questions. Explore your options. Let’s build a plan that fits your life.

Because protecting your paycheck is about more than money, it’s about protecting your peace of mind.

Schedule a consultation today. We’ll help you make a smart move before life forces your hand.

Disclaimer: All content on sjmcares.com and its subpages is intended for informational and educational purposes only. It should not be interpreted as direct financial, insurance, or legal advice. Every person’s situation is unique, call 917-373-0117 to speak with a licensed advisor for personalized guidance.